#1 Element: The Capital Seeker and Capital Provider Relationship

Operating a business is one of the most exciting and adventurous activities in society – it is also one of the loneliest. Developing concepts, pursuing markets and generating commercial activity and productivity usually result in business growth, which is beneficial to the owner (the entrepreneur) and society in general.

Entrepreneurial ventures are distinguished from other small businesses in that they define themselves by their growth potential, vision and their use of innovation, rather than by their current size, to realise their vision. In order to realise their vision, most successful entrepreneurial ventures develop a clear strategic direction, articulated as a Business Plan.

Not all businesses need equity investment nor are they attractive from an investor’s point of view. Most small businesses are lifestyle businesses, which provide a comfortable standard of living for their owners, as well as considerable job satisfaction and an agreeable way of life. These businesses are unlikely to seek external funding, nor are they likely to provide the potential financial returns to make them of interest to an external investor.

Informal venture capital is equity capital provided directly to new and growing unlisted businesses by high net worth individuals – usually known as Business Angels, acting as individuals or as part of informal syndicates. Investing in small and medium sized businesses can be exceptionally financially rewarding. It is also exceptionally risky. An investor is always attracted by opportunities that maximise rewards and minimise risk. The presence of a comprehensive Business Plan assists in lifting the ‘comfort level’ for potential investors, when it addresses the key issues that are pertinent to them as investors when considering investment in a business. Since investors are usually investing their own money, they can be expected to be diligent with their investments and preparatory research. Therefore, unless a business can create this ‘comfort level’, it may be forced to seek alternative methods of achieving its desired growth.

Commercial activity by private investors complements the formal venture capital industry by providing smaller amounts of finance at an earlier stage than most venture capitalists are willing, or able, to invest. It helps take the investee businesses to the point at which they may be potentially attractive to the venture capitalist. This creates a stepped process of funding growth for developing entrepreneurial businesses.

Before looking for informal venture capital from an investor, a business must provide a positive response to the following questions:

- Does the business have the potential to achieve significant profit growth over the next 3-5 years?

- Can it be demonstrated to potential investors that the business has a unique selling proposition (USP) that distinguishes its product and/or service from that of its competitors?

- Is the entrepreneur prepared to raise finance to turn this growth potential into reality, by reducing their share of the equity in the business?

- Is the entrepreneur prepared to accept management input, and possibly share or lose control of the business?

The key to profitable business growth is usually, quite simply, a combination of creativity and money – growth stagnates when creative individuals are deprived of financial resources. This simple equation assumes that management and planning are well structured and in place. The aim of this document is to prepare potential investees and their business, for the inevitable diligent scrutiny of a potential investor who can provide the necessary finance to support that growth. Undertaking the writing of a Business Plan will assist the entrepreneur to adopt a managerial mindset and identify and articulate a vision for the business. At the very worst, the process required to create a Business Plan will force the entrepreneur to think about and question a variety of issues relating to the business. This can only prove beneficial in the long term. In effect a development tool providing strategic direction is being created and articulated for the present and future management of the business to implement.

Business Angels

The term ‘Business Angel’ evokes an image of benign and benevolent beings, charitably supporting businesses to a profitable and fulfilling existence. Business Angels are definitely not business philanthropists – they are investors, nothing more, nothing less! They are usually high net worth individuals who, although prepared to take calculated investment risks, are prudent in their decision making, and monitor their investments closely – in other words, they are selective investors. They may choose to be physically active, or passive, in the business, but can be expected to frequently offer opinion based on their own commercial acumen and expertise. The entrepreneur may not necessarily solicit that opinion! However, any input from an investor is designed for the benefit of the shareholders, of which they are one!

The typical private investor will generally commit between $10,000 and $500,000 to a single equity investment. There are however, numerous investors who will invest larger amounts either individually or in syndicates of informal investors. They invest in almost all industrial sectors and at all stages of business development, but primarily in start-up, early and expansion stages, and characteristically have a preference for investing in companies located close (within 200 kms) to where they live or work. Most investors tend to invest in an industry with which they are familiar and in which they have direct commercial experience. It stands to reason that investors are unlikely to invest in an industry in which they are inexperienced and have little empathy for.

In certain respects, investors act like professional venture capitalists and corporate investors, in that investments are made primarily for financial reasons – for a potential capital gain. Frequently investors may be motivated by the opportunity to make a strategic investment which is complementary to an existing venture or service – although this role would be predominantly expected of Corporate Investors. There are non-financial investment motives too, notably the opportunity to play an active role in the entrepreneurial process, and the fun of making informal investments – these can be important secondary motives for an investor.

Investor Expectations

The key factors which investors take into account when assessing an investment opportunity are:

- The expertise and track record of the entrepreneur and management team.

- Evidence of market focus and concentration on what the business does ‘best’!

- The characteristics and growth potential of the market.

- Evidence of customer acceptance of the product/service.

- The ‘fit’ between the characteristics of the business opportunity and the investor’s own investment preferences.

- Appreciation of investor needs – particularly exit and harvest strategies.

- Proprietorial position – any sustainable market advantage, such as patent, copyright etc.

Likewise, key investors ‘turn off’ are:

- Product orientation – in love with the product and not the market!

- Projections which deviate from industry norms.

- Unrealistic growth projections – demonstrating a lack of understanding of the parameters of the market. As a rule, businesses do not reach a public listing within 5 years, despite the best efforts of the entrepreneur.

- Inadequate funds requested. In the eyes of an investor, this demonstrates a lack of understanding of cash flows and resource requirements for growth. At the very least calculate cash flow requirements for 2 years growth.

Target Your Investor

The Business Plan should be written to attract a particular type of investor. International research indicates that there are 4 distinct types of private equity investors. Each of these have distinctly different levels of investment activity, invest for different reasons, are sourced from contrasting business backgrounds and contribute uniquely to their selected venture. The investor profile best suited to the enterprise should be selected, and the Business Plan styled to suit that particular investor profile. Four investor categories (with self explanatory ‘titles’) are:

- Entrepreneur Investors: as the name implies, highly entrepreneurial and more comfortable with risk than most. Likely to be involved in a number of ventures and active in all, bringing substantial business acumen to projects and likely to be large investors. Generally not looking for long-term commitments, but to provide significant added value to a business. These investors are excited by the challenge and sense of achievement in creating successful businesses.

- Wealth Maximising Investors: simply motivated by the bottom line. Highly motivated and entrepreneurial, they predominantly seek relatively short-term investments. Will be either passive or active in a business, but normally will be very clinical and emotionally detached when making critical decisions. Prepared to invest heavily in a business if returns deemed worthwhile.

- Income Seeking Investors: usually smaller investors seeking a full-time position in a business. Looking for long term commitment, adding significant value to the venture. Generally not big risk takers, preferring to grow a business that can sustain its longevity, than maximise today’s opportunities at the expense of tomorrow.

- “Mentor” Investors: those investors looking to ‘put something back’ into society by taking an investor / mentor role with SMEs. Usually highly active and capable of large investments, they are motivated by a sense of ‘social responsibility’. They are likely to be involved in a number of ventures, involving substantial ‘cross – fertilisation’.

The previous summaries are simplified generalisations, and not designed to hide the fact that investors are predominantly motivated by maximising their investment. It is fair to assume that all investors will require a dividend in excess of an investment placed in a bank term deposit or similar. To this end a minimum Return on Investment (ROI) of +20% will be expected.

Other characteristics:

- Many private equity investors are prepared to accept lower returns than a venture capitalist as they are also motivated by non-financial considerations.

- Most are minority shareholders (it is unusual for an entrepreneur to lose permanent control of the business to an investor).

- They are likely to make more rapid investment decisions than a venture capitalist or Corporate investor, particularly if they are considering investments in industry sectors in which they have experience and so will spend less time and money on a formal due diligence process.

- Most are prepared to keep their investments for at least 3-5 years and very often longer. However, they are likely to want to establish at the outset how and when they can expect to realise their investment. Expected exit routes include company share buy-back schemes, the use of available secondary market mechanisms, trade sale of the business or a market listing.

- Investor’s pockets are not likely to be as deep as those of venture capital firms and so they may be unwilling, or unable, to provide subsequent rounds of finance. Further activity in the capital raising market may be required. This is often where a venture capitalist steps in. Approximately 30% of businesses currently supported by venture capitalists in Australia were originally financed by a private investor.

Control Test… Do You Pass?

Most investors characteristically do not want control, although understandably they wish to protect their investment. Their level of involvement may be varied, from a daily hands on approach, to at the very least board representation (directorship). Issues of control (voting and financial) need to be determined at the negotiating table (preferably following professional advice). However, regardless of the share distribution, from an investors perspective if an entrepreneur is doing a good job resulting in increased market share, growth and/or profits, then control is generally not an issue.

Confidentiality

Entrepreneurs may be concerned that publicising their business through a matching service or similar may stimulate competition or, worse, lead to their ideas being stolen. If they are identified, the competition may be alerted as to their plans. These are legitimate concerns, to which there are two different scenarios:

Scenario One: If entrepreneurs seek an equity partner without utilising the public platform offered by matching services, they are obliged to approach individuals within their own networks, explaining the investment opportunity to each potentially interested investor.

This can be an extremely lengthy process, as:

- Investors have to be identified;

- Information provided and;

- Interest ascertained; before

- Negotiations can proceed.

The process can be an exhausting and psychologically depressing experience as each of the four separate stages allow for rejection. The entrepreneur is also limited by the extent of their networks. Entrepreneurs managing growing businesses can ill afford the time required to attract investors, particularly as this requires time away from the business.

An entrepreneur’s search for an equity investor is also hampered by the fact that private investors characteristically prefer anonymity to avoid being inundated by poor quality investment proposals.

With this process there is a real danger of taking the first equity partner that makes an offer. This person is not necessarily right for an individual business.

This process also has severe legal restrictions, in that only a maximum of 20 investors in any 12-month period can be approached with an “offer” If more than 20 prospective investors are expected to be approached, then Corporations Law requires the raising of a Prospectus. Matching Services and Business Introductory Services are the beneficiaries of a Class Order Relief from ASIC to the effect that they can promote investment opportunities to an unlimited audience – without the requirement of a prospectus.

The legal environment can be complicated and can easily be inadvertently compromised. Readers are strongly encouraged to seek appropriate legal advice as to their rights regarding Corporations Law.

Scenario Two: by utilising a Matching Service, when published (in whatever form), the entrepreneur’s business is exposed to as many qualified leads, and as quickly as possible, through that Matching Service’s distribution network.

Promotion by (for example) the APCX provides real added value for both the capital seeker and prospective investor, as it provides an immediate screening process, through the initial “investment profile” which identifies similarities between the entrepreneur’s investment requirements and a prospective investor’s preferred investment criteria. The initial “match” can be reinforced by the opportunity for the prospective investor to access further information supplied by the capital seeker, by, for example, a Business Plan summary, customer testimonials and verification documents (sponsor documents), such as an audit report.

By utilising a Matching Service, the first three steps of the process – identifying investors, providing information and ascertaining interest – are immediately (and legally) accomplished in one action and an exceptionally wide, but qualified, audience is targeted. It is likely that more than one investor will express interest. Consequently, the entrepreneur and/or their professional representative, is in a position to select the investor that offers the ‘best fit’ for their business, or offer smaller parcels of equity to a number of prospective investors. Having more than one offer for finance provides an opportunity for the entrepreneur to negotiate from a position of strength, perhaps securing a better deal than that initially offered.

The issue of confidentiality will never go away, although the signing of ‘commercial in confidence’ agreements for prospective investors does assist in this regard. Most Matching Service’s ensure in their process that:

- The business seeking capital is unidentified;

- The speed and scope of the exposure minimises the risk, and

- Confidential material is not exposed in any form.

The entrepreneur has final veto over the content that is published and to whom more detailed information is provided – in other words the entrepreneur has total control regarding the extent of information provided to the market.

Due Diligence

All prospective investors will undergo some form of due diligence, which will vary in their degree of scrutiny. Inconvenient as it may appear, this is in fact a positive sign that investor’s are prepared to take the trouble to investigate, reflecting their level of seriousness.

Due diligence is essentially the investigation of the facts of the business and investment opportunity. It determines if the Business Plan is a true reflection of the business through a process of auditing accounts, industry analysis, interviews and other investigative techniques. The emphasis is on an understanding and quantification of the inherent risk involved. Often an expensive (for the investor) and intrusive (for the entrepreneur) exercise, the intensity of the due diligence process will vary from investor to investor.

Attempts in the Business Plan to ignore or gloss over weaknesses in the business will only reflect badly on the integrity, experience, talent and competence of the management team, thereby affecting the goodwill of prospective negotiations.

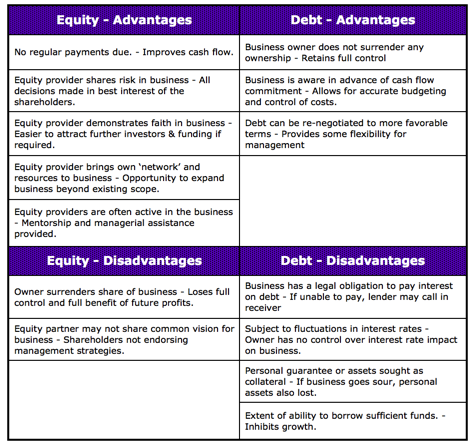

#2 Element: Equity vs. Debt

Most businesses, regardless of their growth stage, require an outside source of capital at some stage. Usually there are only two forms of capital available – equity or debt. There is a clear distinction between the two.

Equity capital is money invested in a business in exchange for a share of that business. The equity investor is committed to the business in both the good and bad times, sharing in both the risk and reward of the venture. In the case of business growth they are entitled to a share of both the profits and capital growth. In the case of failure they undertake the risk of losing their investment. Friends, family, “Business Angels” and Venture Capitalists are common examples of equity investors. Usually equity providers invest their own money.

Debt capital is money invested in a business, in exchange for the legal requirement to repay an agreed sum on a regular basis, until the initial sum and interest is returned in payment. Usually, collateral in the form of assets equivalent in value to the loan sum is expected as guarantee, and can be possessed in the case of an inability to maintain payments. Banks and other financial institutions are the usual examples of money lenders. Lenders are rarely committing their own money.

The table below provides a comparison between equity and debt capital from the perspective of a business:

#3 Element: The Business Plan

Why Write a Business Plan?

In this context, a Business Plan is a selling document that conveys the excitement and promise of a business to any potential backer or investor, as well as providing a sense of what the entrepreneur expects to achieve with the business within a given time frame. It clearly articulates the product and/or service the business provides, and is supported by financial statements, managerial analysis, marketing strategies and opportunity research.

Basically, the Business Plan identifies ‘what’ it is that the business does; ‘why’ it is doing it; ‘how’ it is doing it and ‘when & where’ it is doing it!

From an investor’s perspective, a Business Plan provides a clear understanding of the business and its future aspirations and strategic direction, and can be used as a means of placing a financial valuation on both the business and the opportunity. There is no single obvious model as to how a Business Plan should be drawn up, as each business is unique. The following guide is designed to address most generic issues a prospective investor would be expected to analyse regarding a business.

Entrepreneurs are encouraged to utilise this guide as an analytical tool for their business, as it is structured in a way that creates a comprehensive overview of the business, addressing all the relevant key issues, regardless of whether the business is based on a product or service. Depending on the nature of the venture, the Business Plan would be expected to be somewhere between 10 to 30 pages long, with an avoidance of spreadsheet and ‘technical jargon’ overload.

When wishing to attract an investor, the Business Plan is designed as a ‘selling document’ and must consequently demonstrate a strong market rather than product/technical focus. There is no need at this stage, to provide too much information regarding the ‘nuts and bolts’ of the operation: However, having said that, this is not a half-hour exercise. A potential investor will probably require further due diligence if, after reading the Business Plan, they are still keen on investing in the business. If the business has any letters of endorsement from an influential industry ‘player’ or has received government assistance in any way, highlight these in the Business Plan, as they are regarded favourably by investors.

APCX encourages each entrepreneur to seek the assistance of a professional adviser (accountant or similar) should they need any advice or assistance with the construction of the Business Plan. Preferably seek advice from someone who has capital raising experience.

The presentation of the Business Plan is a reflection of the dynamic commercial environment of the business and should be written on a word processor (computer), which will provide a document that can be readily amended (Business Plans are evolving documents and should be reviewed regularly – at least every quarter), should the need arise.

In this instance, the Business Plan is being written for the express purpose of raising equity capital, so a number of potential investors are the ‘end readers’. The writer should try to put themselves in an investor’s shoes. What is attractive and unattractive about the business? What is the opportunity? Why would someone invest in this business? The plan should be written for the end reader – the investor. Stand back, be Objective!!!

Contents of the Business Plan

The following guide covers the headings and subject matter of a comprehensive Business Plan targeted at a potential investor to analyse.

1. Executive Summary

Probably the most crucial passage of the whole document. This must be written in a way that conveys the entrepreneur’s excitement and enthusiasm for the venture, enticing the reader to read on. The reader (or investor) will form an impression of the whole business concept from the Executive Summary and, if not sufficiently interested or impressed, may choose not to read any further – an investment opportunity lost. It is important to recognise that an entrepreneur is more likely to attract an investor, if they deliver information an investor wants to hear! However this must be done realistically without misrepresentation in a clear and concise manner. To this end prospective investor’s will be asking themselves the following key questions:

- What? What is the business/product/service they are being asked to invest their money and time into?

- Why? What makes that business so special and competitively unique?

- How Much & When? What does the entrepreneur want from an investor, both in financial and “physical” commitment? What is the extent of the market/investment opportunity?

- What For & How Long? What are the potential rewards for the investor ie the “what’s in it for me” factor? When can the investor expect to reap the rewards of their investment, through harvest and an exit? How is the exit expected to be achieved?

- Who? Who is the investor being asked to invest in? What evidence is there that the management team is capable of achieving their aspirations?

- How? What strategies are to be implemented to achieve the same aspirations?

- What Can Go Wrong? How sensitive is the entrepreneur to possible risk factors? How realistic is the opportunity?

This information must be clearly imparted within the first page in order to maintain investor interest, and to provide an appropriate overview for the investor. If, after reading the Executive Summary these issues have been clearly understood by prospective investors, then a major hurdle in the ‘selling’ process has been negotiated.

The Executive Summary must identify how much capital is being sought and potential return to an investor. An outline of ‘the deal’ (what the equity is worth in company shares) may be included, although that is a personal decision, which may be introduced at a later stage in negotiations.

The Executive Summary should also identify the type of investor being sought. Is it preferred that the investor be active or passive in the daily operations of the business? Are particular skills, such as financial, marketing or legal desired in the Investor?

Although cited at the beginning of the Business Plan, the Executive Summary is always the last ‘passage’ of the document written. A document cannot be summarised until it’s actually been written.

2. Table of Contents

All documents should have a Table of Contents. This provides an overview of the issues covered in the document and an easy point of reference.

3. Industry

An overview and history of the industry in which the business trades should be provided, highlighting any particular trends; demand determinants (eg price, service, quality); key sensitivities (e.g. if you are a bricklayer, the number of new housing starts at any given time has a huge impact on the industry); and what motivates people to buy from this industry. Research from public services such as Australian Bureau of Statistics (ABS), IBIS, Dunn & Bradstreet, newspaper articles and Industry Associations may be particularly helpful in this regard.

The market size and growth in the context of the product should be determined. Does it have local, state, national or international potential? Indicate what the market will bear in terms of price and volume.

4. Product or Service

What is ‘it’ that the business does and is setting out to achieve? Can the product or service be classified as a commodity? Highlight what makes the product or service different or unique to the rest of the market.

If any patents, copyright/trade marks or other intellectual property are owned, provide descriptions, concisely stating what they are. If the product is of a particularly technical nature, there is no need to provide all the technical information, as this may be confidential, just sufficient information so that an investor will have a clear understanding of the product’s virtues. Further information can be provided in support documents.

Concentration and focus on a single product/service and market application will generally win favour with an investor. A wide range of products/markets dilutes the considerable time and energy required to pay appropriate attention to marketing. Rather than minimising risk, a wide range of products and/or commercial applications and opportunities, reduces focus, thereby increasing risk.

A demographic and geographic profile of customers should be provided – who buys and uses the products or services. How does the business fit in the ‘Value Chain’ -i.e. the process of steps a product takes from its creation until it reaches the end user or consumer.

If the business is a manufacturer, the manufacturing strategy should be explained, including the ability to source regular supply. How strong is the relationship with suppliers? Are any supplier relationships exclusive? How many suppliers are there?

Payback Period: What is the user benefit of the product / service, and why would someone buy the product/service? Does it save costs for the end user, if so, how much over what period? Is this payback period a significant marketing point? Can the payback period be calculated in reduced costs (labour, rejects, inventory etc) or increased revenues (productivity, capacity, efficiency etc)? Are there non-monetary benefits – health, convenience, time saving, environmental, appearance etc.

5. Opportunity

What is expected to be achieved? Why is this going to happen? Who or what is the target market and what are the relevant market share projections? A realistic approach should be adopted, substantiating all projections with reasoned logic, if possible supported by research and market statistics.

Where is the opportunity taking place and how long can the business expect to have a market edge? Is there a sustainable competitive advantage?

6. Competition

The competition should be identified – their market share, resources and most importantly their anticipated reaction to the proposed actions of your venture. Create a table of major competitors highlighting their strengths and weaknesses.

Opportunities to form joint ventures or strategic alliances with any other industry participants should be identified. What are the barriers to entry (if any) and exit for new entrants to the market?

7. Sales, Marketing and Distribution Strategies

Marketing is strategy, sales are tactics. How does the business expect to achieve its aims? How broad are networks and channels of distribution? Is there anything innovative in the approach to sales, marketing and distribution.

Why does the business enjoy repeat business? What is the sustainable customer satisfaction? How is the sales team organised? Is there an incentive programme? How will ‘gun’ sales staff be attracted (head hunted?) to the venture?

Consider the effectiveness of the distribution network and the relevant profit margins at each point in the value chain. Can methods of maximising profit through the current system and expanding into new market opportunities be identified?

8. Management

It is often said that the three main ingredients to business success are 1) Management; 2) Management and 3) Management! All available research clearly indicates that management is the main non – financial factor that influences an investment decision. Ultimately people invest in people, as somebody has to provide the necessary expertise and drive in order to commercialise the product or service.

Summarised CV’s for the management team should be provided, with particular emphasis on their ability and skills in relation to the business project in question. Is the management team results orientated? Identify the key personnel outside the management team, and explain the staff motivation (money, work, achievement, pride etc). Is the internal culture unique in any form? These issues are crucial, as investors need reassuring that the management team and staff will retain their commitment in tough times.

To a prospective investor, quality of management is essentially a function of 4 components:

- Integrity: Private investments in companies are founded on trust.

- Experience: Have those with the responsibility with guiding the business, have the necessary experience in the relevant commercial environment? Are they capable of facing the pressures of conflicting priorities associated with a dynamic business environment?

- Talent: Intangible, but instantly recognisable. Does the management team recognise its weaknesses, and what steps have been taken to address them? Do they know what they don’t know! Is the management team capable of meeting the challenge ahead?

- Competence: Empathy with the industry and recognition and understanding of the industry drivers. The skills set of the management team.

This section does not have to be particularly long, but must reassure the investor of the entrepreneur’s and the management teams core competencies and ability to achieve the projected milestones. How will individual specialities complement each other to the advantage of the company?

The legal structure of the business, identifying all shareholders and directors, should be presented in this section. Likewise the issue of the entrepreneur’s (and management team) financial commitment to the project – usually referred to as ‘hurt money’. Investors will always favour a project where the entrepreneur has a significant financial downside to the venture should it fail.

It is appropriate at this stage to identify the investor’s anticipated role in the venture, either active or passive, and what investor reporting mechanisms will be introduced. At the very least an investor would expect a position on the board as a non-executive director. Detailed information as to the make up of the board (anticipated or otherwise) must be provided.

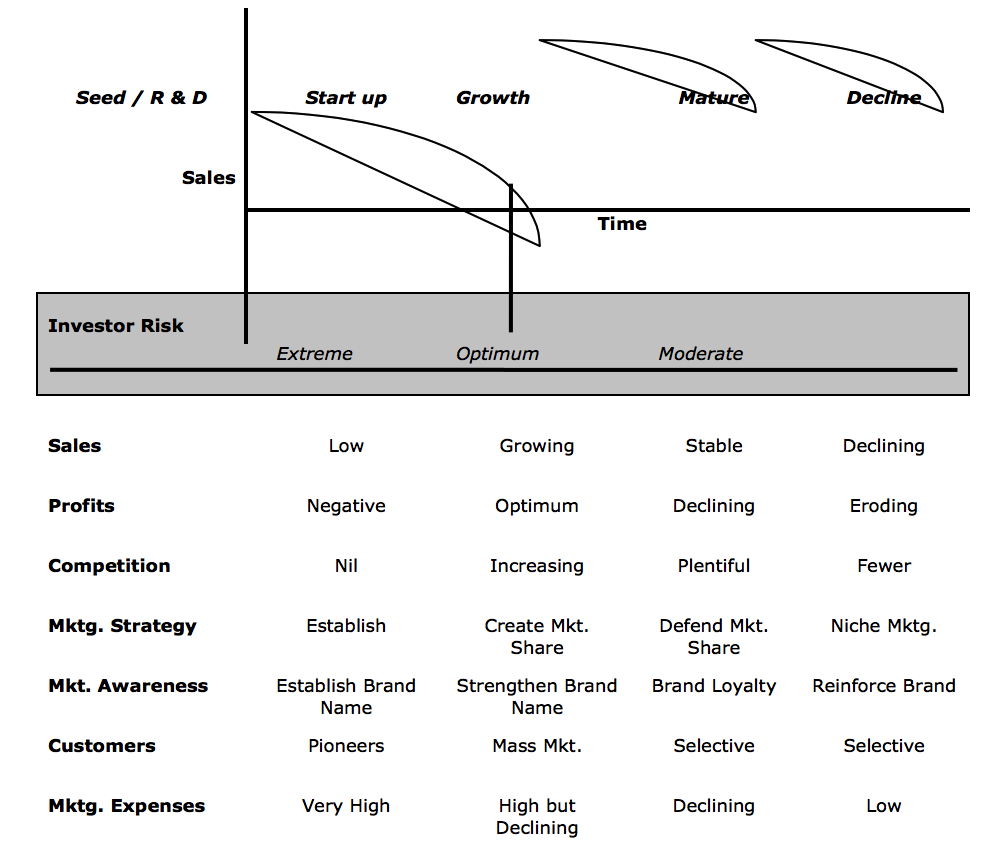

9. Product Life Cycle

Determining the position of the product and/or business and the industry in their respective life cycles is of enormous benefit to any investor, providing a simple graphical representation of the stage in a product, service or business’s life.

The above is a generic model of a typical product/service/business life cycle. Although exaggerated, it clearly demonstrates the four different phases experienced under the life cycle concept.

Investors are unlikely to be attracted to a business entering into a mature or declining phase, as the profit returns would be expected to be moderate at best, although the risk is relatively minimal. Conversely, a project in seed or start up phase offers no guarantees and is full of risk. Equity negotiations would be expected to reflect this risk in favour of the investor.

Ideally, an investor prefers to invest at the lower end of the growth curve, where there are some proven sales and the market is beginning to gain momentum. Although there is still an inherent risk in any investment, the opportunity to maximise sales and profits and benefit from the growth is usually sufficient motivation to commit to an equity position.

Not all companies follow this model; however by being able to recognise patterns and adapt strategies accordingly, a business can extend its periods of growth beyond the accepted norm. Being able to interpret industry trends and implement proactive strategies demonstrates a management ability that is extremely attractive to any prospective investor.

10. Financials

Businesses financial projections are the result of its strategy and planning. The figures must be believable and realistic, but sufficiently attractive to win investment. Financial forecasts are viewed by investors as a yardstick by which to judge performance. From these projections, shareholder instruments such as bonuses, royalties, options, buy back schemes, as well as a company share valuation, can be determined.

Four basic financial statements are always required: Balance Sheet, Cash Flow, Profit and Loss and Break-even Analysis. Generally the main focus is on the cash flow, followed by the P & L. Usually assets are not as important to an investor, to whom cash flow is king – lack of cash flow is normally the reason businesses seek an investor!

Growing bodies need to be fed, and a business that experiences rapid growth devours cash. It is not uncommon for growing profitable businesses to experience serious difficulties due to a precarious and inconsistent cash flow. A comprehensive cash flow statement will clearly demonstrate financial assumptions: eg debtor days, period expenditure, taxes etc. Often it is not the projected figures that are important, but more the reasoning behind the assumptions. Assumptions must be clearly stated and be able to be substantiated.

Not only does a financial analysis provide a reality check in terms of costing, it also provides an analysis of timing of events and their impact on the business. Expect an investor to immediately discount sales figures by as much as 20% and lift costs by a similar figure during their due diligence. Can the business sustain this? Expect an investor to only analyse a medium and worst case scenario.

Financials should be provided on a computer disk, formulated on a spreadsheet; allowing a number of ‘what if’ permutations to be calculated. Significant credibility is generated if these have been prepared by a professional (such as an accountant) with capital raising experience. Graphs and tables are an asset in this area, as they can simply explain and convey complex financial permutations.

If possible, Balance Sheets and P & L Statements for the previous 3 years and the current trading period (quarter). Most importantly, monthly cash flow projections for the next 12 months, quarterly for year 2, and annually for the projected period of the investment (5 years?) should be provided. Projected P&L’s for the same period are expected. Include gross margins in the P&L Statement. Quantifying future projections is at best an inexact science, hence the key assumptions behind the financial modeling must be articulated.

An investor must have a means of measuring their investment. This is usually achieved through the calculation of Return on Investment (ROI) or Internal Rate of Return (IRR). This may be linked with accounting controls and an audit mechanism, offering protection for the investor. This may take the form of monthly accounts, management reports, disaster milestones, board structure, veto rights etc.

Regardless of the business, a Break-even analysis should be presented. This is crucial information to any business, and not unique to manufacturers. It is very difficult to make a sustainable profit if there is no understanding of the concept of measuring fixed and variable costs.

Generally, predictive financial statements that are realistic (ie objective) are beyond the skills of entrepreneurs. Seek professional help, preferably from someone with capital raising experience.

11. SWOT & PEST Analysis

SWOT – Strengths, Weaknesses, Opportunities and Threats

The strengths and opportunities of the business or product/service should already be apparent, as they have been discussed at length elsewhere in the Business Plan. However have weaknesses been identified? Perhaps technical skills are not as developed as marketing acumen, and the business survives by delegating or contracting out these tasks. Are limitations or flaws with the business/product/service recognised? An investor can be expected to probe these areas – far better that they be brought to their attention, with any corrective actions identified, than an investor ‘discovering’ flaws in their prospective investment during the due diligence process.

It is recommended that a table be created for the SWOT analysis. There should not be concern about identifying weaknesses and threats, but a point should be made of stating a strategy to counter any threats (contingency plans), and correcting any weaknesses.

PEST Analysis – Political, Economic, Social and Technical.

These are macro issues over which it is unlikely the business has any direct control. However, maintaining an interest in and monitoring issues and trends that may impact on the business is crucial. The business may be in a position to recognise and take advantage of a ‘window of opportunity’ before the rest of the market, or conversely take corrective action or implement strategies that will pre-empt an event that may have a negative impact on the business. Can the business be unduly influenced by political legislation or changes of Government? Can the technology be superseded?

12. Critical Success Factors

How is the success of the venture measured? Turnover milestones? Proposed market share achievements? Specific achievements such as an IPO or trade sale? List the key success factors (no more than 5) of the venture, and the anticipated time frame of achievement. Support this list with the broad strategy required to achieve each key success factor.

Lucky 13. Exit Strategies

How can an investor protect their investment? When can an investor withdraw their association with the business, preferably maximising their investment?

Generally, investors (private or institutional) do not wish to invest in a venture for life, or for any sustained period. Three (3) to five (5) years investment life is the norm, hence investors want to know prior to their investment commitment how and when they will realise the proposed investment.

What is the strategy identified in the event of things no longer going to plan? The confidence level of the investor should be lifted by offering some contingency strategies should things go wrong. Do not think it can’t happen – a Business Plan is no guarantee of success. Unexpected events can destroy a business – changes in Government Policy, dock strikes, stock market crashes, extremities in weather conditions etc.

14. Assumption Statement

The Assumption Statement clearly defines the environment and conditions in which it is anticipated the venture will operate. This is crucial for any realistic assessment of risk made by the prospective investor.

15. The Deal – The Benefits to the Investor.

There is an old saying – Tell them what you’re going to tell them (Executive Summary), tell them (Opportunity) and tell them again! This should be adopted for the Business Plan.

What are the main reasons someone should invest in the business? What are the benefits for the investor, both quantifiable and intangible?

Not all investors will want to maintain their investment in the company. The period of investment is obviously a negotiable issue, but the entrepreneur must be aware that investors will usually want to harvest their investment at the agreed rate within a certain period. This should be born in mind when negotiating milestones and ROIs.

From the investor’s perspective, performance is reality…

16. Information Memorandum

Name and address details of Accountant, Solicitor Bank, and other key entities involved in the venture.

Other Readings

This Business Plan guide is a general indicative overview of the issues that an investor can be expected to address. In no way can this guide be interpreted as a conclusive format and list of content for Business Plans. There may be a number of issues peculiar to the industry or unique to the business – these should be emphasised.

There are a number of excellent books on the subject of writing Business Plans. These are mostly available from libraries or academic bookshops or from a local business advisory centre. Some are better than others, some are industry specific, some are just lists and headings. Likewise there are a wide variety of courses, offered by academic institutions, government and private companies. The quality of content will obviously vary, but it is logical to assume that those offered by people with direct capital raising experience are likely to be more focused and productive. There are also numerous Business Planning software programmes that are available. Again, there are significant variances in quality and content. If unsure seek advice from a professional advisor such as an accountant, or APCX or similar industry body / association.

Basically a Business Plan is just common sense, and in this instance an articulation of the venture for the benefit of a prospective investor.

Reference and Article Sources:

[1] David Masters, Chief Architect & Founder at APCX.

[2] The Private Equity Council – Sydney 1999.

[3] R. Inglis – Amgun Holdings. ADCAL Conference – Sydney 1996.

[4] This is applicable at the time of writing (Feb 1999). The CLERP proposals are expected to be legislated in June 1999,radically altering the current legal environment. One such change will be changing the 20/12 rule to apply to 20 ‘acceptances’ as against 20 ‘offers’.

[5] This applies only to investors seeking to individually invest less than $500,000. Readers are advised to seek professional legal advice as regards their capital raising activities in relation to the Corporations Law.

[6] Australian Securities & Investment Commission

[7] ASIC: Corporations Law – Subsection 1084(2) – Exemption – CO 97/2329 and CO 02/0273

[8] Under the current legislative environment (Corporations Law) there are some restrictions in relation to the promotion of information relating to the ‘offer’ of the investment opportunity. The reader is strongly advised to seek appropriate legal advice regarding their status in relation to Corporations Law.

You must be logged in to post a comment.